" height="19.593489627012634px" id="HZMnoshln" transform="translate(35.667 1.777)" width="65.54153019346582px"/><path d="M 0 0.017 C 2.315 0.103 4.878 -0.071 7.193 0.036 C 7.468 0.279 12.481 5.793 12.556 5.958 C 11.717 6.005 10.736 5.956 9.888 5.958 C 8.409 5.961 6.923 5.977 5.446 5.957 C 4.793 5.44 4.259 4.69 3.684 4.077 L 1.651 1.879 C 1.049 1.235 0.525 0.741 0 0.017 Z" fill="rgb(0, 190, 110)" height="5.978734113643265px" id="B_ZyWaY8J" transform="translate(12.847 17.922)" width="12.556331656472807px"/><path d="M 18.85 0 L 25.936 0 C 24.823 1.198 23.694 2.514 22.583 3.726 L 11.098 16.3 L 7.002 20.802 C 6.307 21.56 5.61 22.392 4.847 23.07 C 3.802 23.997 1.958 23.832 0.982 22.861 C 0.429 22.31 0.203 21.736 0 20.995 L 0 4.033 C 0.736 4.729 1.513 5.612 2.204 6.369 L 5.127 9.559 C 5.157 10.119 5.127 10.896 5.126 11.475 C 5.128 12.703 5.12 13.932 5.101 15.16 C 5.602 14.614 6.075 14.035 6.574 13.485 L 11.831 7.736 C 14.119 5.193 16.502 2.478 18.85 0 Z M 60.302 6.916 C 61.496 6.907 62.723 6.937 63.927 6.935 C 62.687 10.72 61.245 14.453 59.866 18.186 C 59.324 19.656 58.713 21.843 58.009 23.157 C 57.54 24.036 56.936 24.913 56.037 25.37 C 55.493 25.647 54.887 25.798 54.297 25.935 L 52.098 25.935 C 51.91 25.715 52.001 23.361 51.992 22.874 C 54.16 22.932 54.67 22.721 55.309 20.461 L 52.023 11.377 C 51.506 9.944 50.881 8.391 50.444 6.937 C 51.689 6.941 52.935 6.933 54.181 6.913 C 54.393 7.343 54.775 8.624 54.941 9.14 C 55.392 10.543 55.864 11.949 56.361 13.336 C 56.62 14.057 56.993 15.495 57.285 16.127 C 57.802 14.421 58.424 12.752 58.95 11.029 C 59.213 10.164 59.955 7.668 60.302 6.917 Z" fill="rgb(255, 255, 255)" height="25.9350729038176px" id="RJr52Ozxy" width="63.92682320478577px"/></g></svg>)

Blog

FCA AML Fines: Why Data Failures Drive AML Enforcement Actions in the UK

Author

The Kyckr Team

Published

Between 2020 and 2025, the Financial Conduct Authority imposed over £430 million in fines on UK financial institutions for AML non-compliance.

Kyckr’s analysis of 22 Final Notices shows that in 68% of cases, data deficiencies were a material factor. The pattern is consistent. Firms failed not because they lacked compliance frameworks, but because those frameworks ran on bad data.

Why AML Enforcement Actions Are Increasing

The FCA has shifted. It no longer asks whether a firm has an AML policy. It asks whether that policy works in practice.

The test is operational: can a firm obtain, verify, and continuously update accurate customer information?

The penalties for money laundering in the UK make clear that the answer, for too many firms, has been no.

Four failure types account for most FCA AML fines. Each is a data problem.

1. Outdated or Missing Information

45% of AML fines involved outdated or missing customer records. The cases are instructive:

ADM Investor Services International: Maintained a database of Politically Exposed Persons that was out of date. The gap was exploitable. It was exploited.

Gatehouse Bank: Screened shareholders of a special purpose vehicle against an outdated investor list in December 2014.

Ghana International Bank: Did not detect for five years that a business client had ceased trading. Dormant accounts, left unmonitored, become open doors.

The principle holds across every case: bad information produces bad risk assessments. Firms cannot calibrate their AML defences against customers they do not truly know.

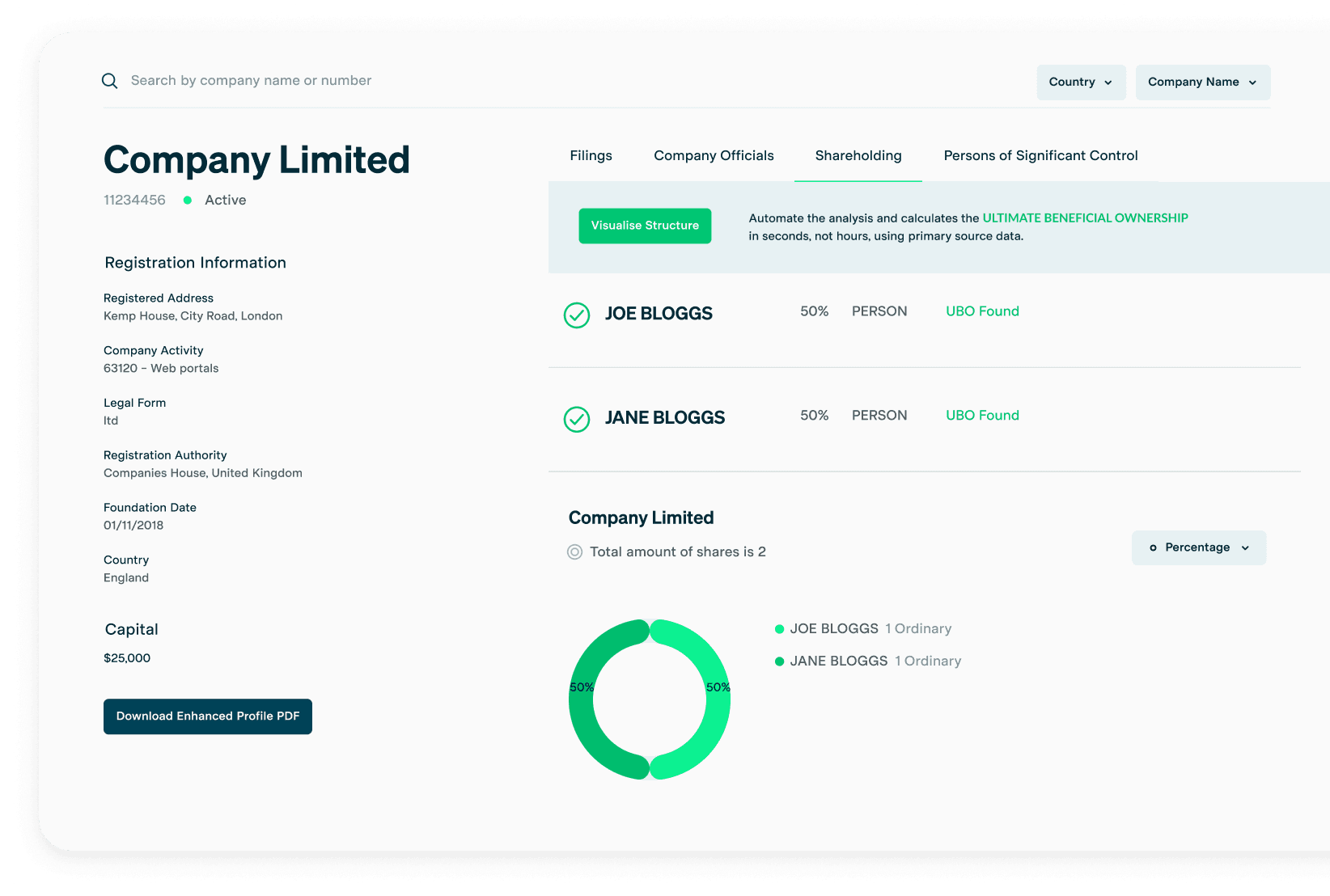

[caption id="" align="alignnone" width="1776"]

How UBO Verify works, calculating UBOs based on live shareholder data extracted from company documents in real-time. [/caption]

2. UBO Verification Failures

32% of FCA AML fines involved failures to identify and verify ultimate beneficial owners. Knowing who controls an entity is not optional. It is the foundation of knowing who you are doing business with.

Monzo: Failed to verify the UBOs of 19,198 onboarded entities. No financial crime was detected as a direct result, but the exposure was real.

JLT Speciality: Did not verify the directors and shareholders of a high-risk entity, nor obtain its Certificate of Incorporation from the Panamanian public registry. The result was that they onboarded a customer who subsequently channelled illicit funds through bribery networks.

Solo Group: Outsourced CDD to the Solo Group itself. Many Solo "clients" were in fact entities controlled by the Solo Group. The brokers did not know this because they had not independently verified beneficial ownership. The Solo Group could not provide an unbiased view, and no one checked.

True UBO verification means more than matching a name to an ID document. It means building an ownership map. It means identifying how entities are linked. The Solo Group cases show what happens when firms cannot join the dots.

3. Weak Source of Wealth and Source of Funds Verification

32% of firms fined failed to verify the Source of Wealth or Source of Funds. Without this verification, enhanced due diligence is theatre. Firms cannot contextualise transactions they cannot explain.

Al Rayan Bank: Onboarded a UK-registered machinery seller ultimately owned by an Iraq-based businessman, which deposited £580,000 in cash despite having claimed monthly instalments of £2,000. The bank could not explain it.

Guaranty Trust Bank: Could not verify the annual turnover of several customers. Transaction volumes were inconsistent with declared wealth. Resources were misdirected toward geographically based blanket risk assessments rather than properly calibrated EDD.

Sunrise Brokers: Failed to obtain SoW and SoF information from Solo clients. Under pressure from the Solo Group to onboard quickly, Sunrise removed the funds-origin question from its KYC forms.

Customer reluctance to provide SoW documentation is a red flag. Removing the question in response is a failure.

4. When Customer Declarations Do Not Match the Public Record

Identification is not verification. Four firms were penalised for accepting what customers said about themselves without checking it against public records.

National Westminster Bank: The SIC code of gold bullion dealer Fowler Oldfield was changed from precious metals to wholesale metals. The change was not aligned with Companies House records. The customer’s risk rating dropped from high to low. The account was excluded from high-risk remediation. Millions were laundered.

Santander UK: Opened an account for a company claiming to be a translation service with an expected turnover of £5,000 per month. Companies House listed a different SIC code linked to financial intermediation. Within a year, £26 million had passed through the account. Similar discrepancies occurred in three further cases involving money services businesses.

Monzo Bank: Customers listed addresses including Buckingham Palace and 10 Downing Street. These were not verified against independent sources.

The distinction between identification and verification matters. Accepting customer declarations without checking authoritative sources creates blind spots.

[caption id="" align="alignnone" width="1644"]

Live company, pulled from official company registries in real time. [/caption]

How to Avoid the Next FCA Fine

The enforcement record is a blueprint in reverse. Every FCA fine points to a specific failure mode.

Most trace back to the same root: firms could not obtain independent, reliable, current data on their customers, or could not integrate it effectively when they had it.

The FCA's standard is clear. Customer information must come from independent and reliable sources.

Yet official company data is fragmented across hundreds of registries, each with different formats and access rules. This fragmentation leads to siloed workflows and missing linkages.

Kyckr Addresses the Root Cause

Through a single API or the Kyckr Portal, firms gain real-time access to more than 300 official company registries, including jurisdictions that are traditionally difficult to access.

This enables:

Instant retrieval of authoritative company documents directly from official registries.

Real-time verification of ultimate beneficial owners based on live shareholder data.

Centralised ownership mapping to identify linkages between entities and individuals.

Continuous monitoring to detect changes in status, directors, or shareholders.

In short: Audit-proof company data, in real time, in one place, from all over the world.

How to Maintain Full Compliance With the FCA

The FCA’s recent fines show what happens when firms rely on outdated files, self-disclosures, or fragmented third-party processes.

Direct access to authoritative registry data allows compliance teams to build a complete, verifiable customer profile at onboarding and maintain it throughout the lifecycle.

In a regulatory environment where 68% of recent AML enforcement cases involved data weaknesses, closing the data blind spot is imperative.